US housing market softening while supply falls in 2023

One of the things we like to watch when thinking about real estate investment is the activity in new residential construction. It’s generally a good forward indicator for pricing and household behaviour. Residential real estate is the largest asset class in the world with commercial slightly behind. Patterns and trends early in the residential construction cycle are impacted by raw material costs, labour and the availability and price of credit.

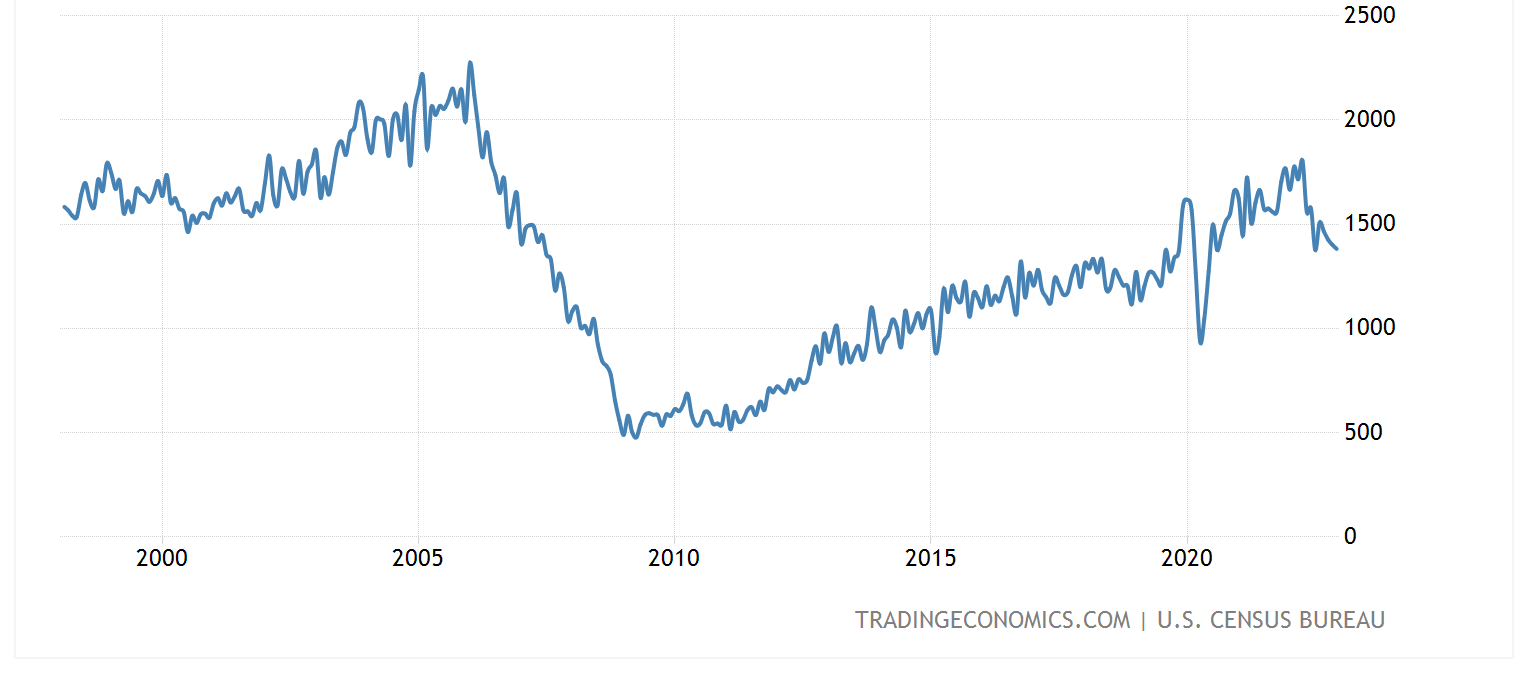

In the US, housing starts measure the activity of newly constructed homes as they progress through the construction and sales process. US housing starts famously peaked at over 2 million per month before the 2009 crash and bottomed at around 500 thousand in the preceding years. They have seen been on a gradual rise.

Housing starts have come off over the past few months, no doubt a response to the rising interest rate environment and uncertainty if the US economy in 2023.

The good news here is that the market is already self-correcting and given the steady increase in supply over the past few years, there seems to be enough housing stock in the market to meet rental and social demand. December housing starts fell to around 1.3 million and we get the January numbers this week, which could show another fall.

We think US housing starts will probably bottom at around 1 million towards the middle of this year, which again is a healthy level of balanced supply and demand. This rate will be half the amount of new home construction experienced before the last blow up, again important for maintaining house prices.

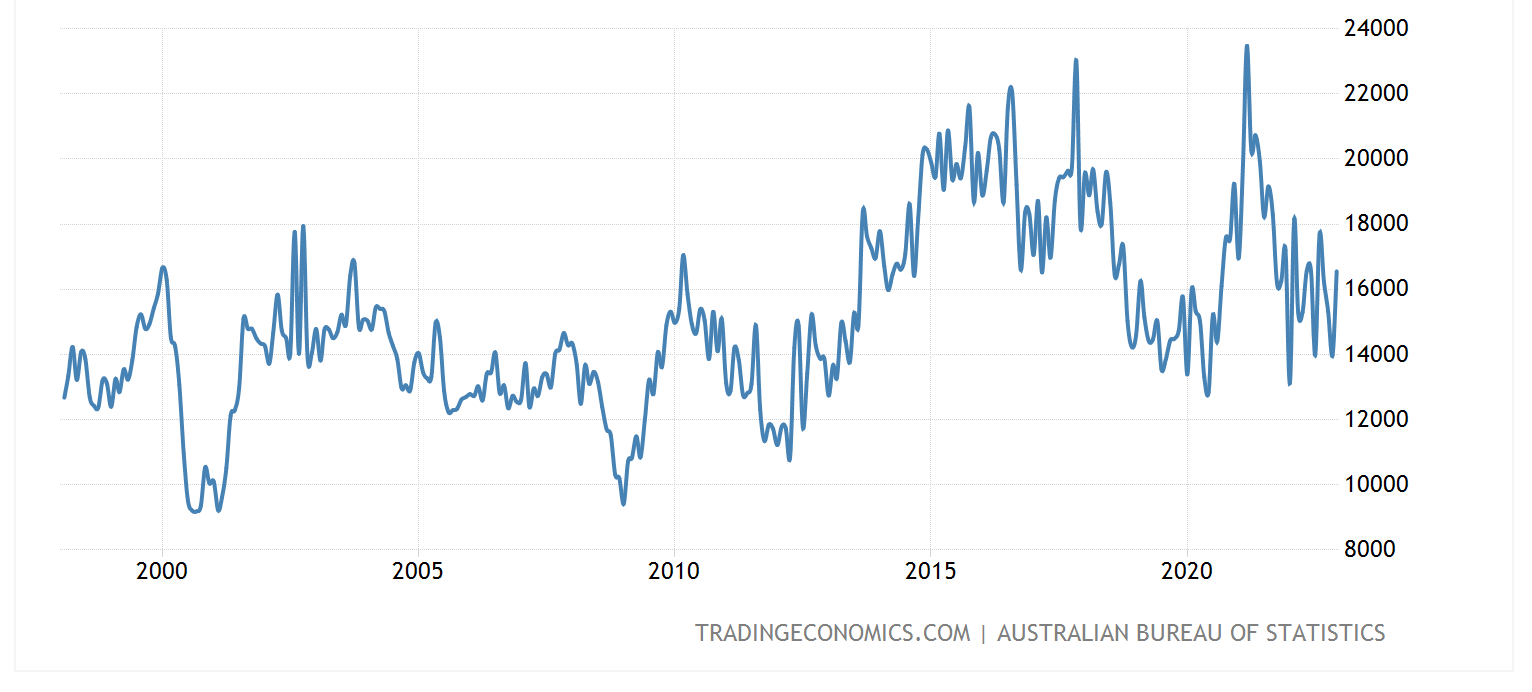

In Australia, the situation is slightly different. We tend to look at dwelling approvals which are slightly different because they don’t necessarily indicate if the home has progressed into constructed. Instead, the assumption is that approvals will eventually proceed to construction most of the time, with some lag. Approvals and permits are our main lead indicator into the future supply of new housing.

Supply has been a lot more constrained in Australia and as you can see from the chart above, we haven’t necessarily had the spike in construction activity seen in America over the past couple of years. In fact, Australian dwelling approvals have been tracking down since the pandemic. We’re now back to an average of around 15 thousand per month, which implies an annual construction run rate somewhere in the order of 180 thousand new homes a year.

Australian housing supply is impacted by zoning, construction costs, a tight labour market and now the impact of rising interest rates. Australian mortgages have a much smaller fixed component than the United States, which means RBA movements are felt quicker and have more impact.

The point is, housing supply is just as important as housing demand in determining where house prices go. Even in a rising interest rate environment. Here are some comments from a real estate conference we attended last week.

Our construction sources in Australia tell us that while building materials have stopped or moderated from rising in price, they are still significantly higher than their pre-pandemic levels.

An unemployment rate in the mid 3% range also makes labour very expensive and rising rates complicate financial feasibilities. We’re seeing a dwindling supply pipeline on the horizon, despite state and federal government initiatives to increasing housing supply.

Official building permit and approval data confirms the same.

So while the US housing supply picture is coming off a much larger base, Australia is still in a very different league and soft to begin with. This explains why house prices might behave differently between geographies and drawing comparisons is fraught with danger.