The Mexican standoff in commercial real estate

Commercial real estate is a loose term for a global asset class that encompasses many, different, types of assets. Put simply, commercial property is anything other than residential. Within commercial, there is a world of difference between the office and logistics markets. Each are driven by different structural themes which were accelerated by the pandemic.

The office market is a big area of risk and our focus in this note. To understand the problems with office assets, we need to understand the process of valuation.

Larger assets are generally less liquid, compared to say residential real estate and so the value is more opaque. As interest rates have risen, real estate values have generally fallen unless rents and income have risen at the same or even greater pace. That explains why residential real estate prices are holding up relatively well. Residential rents are rising quickly, offsetting funding pressure.

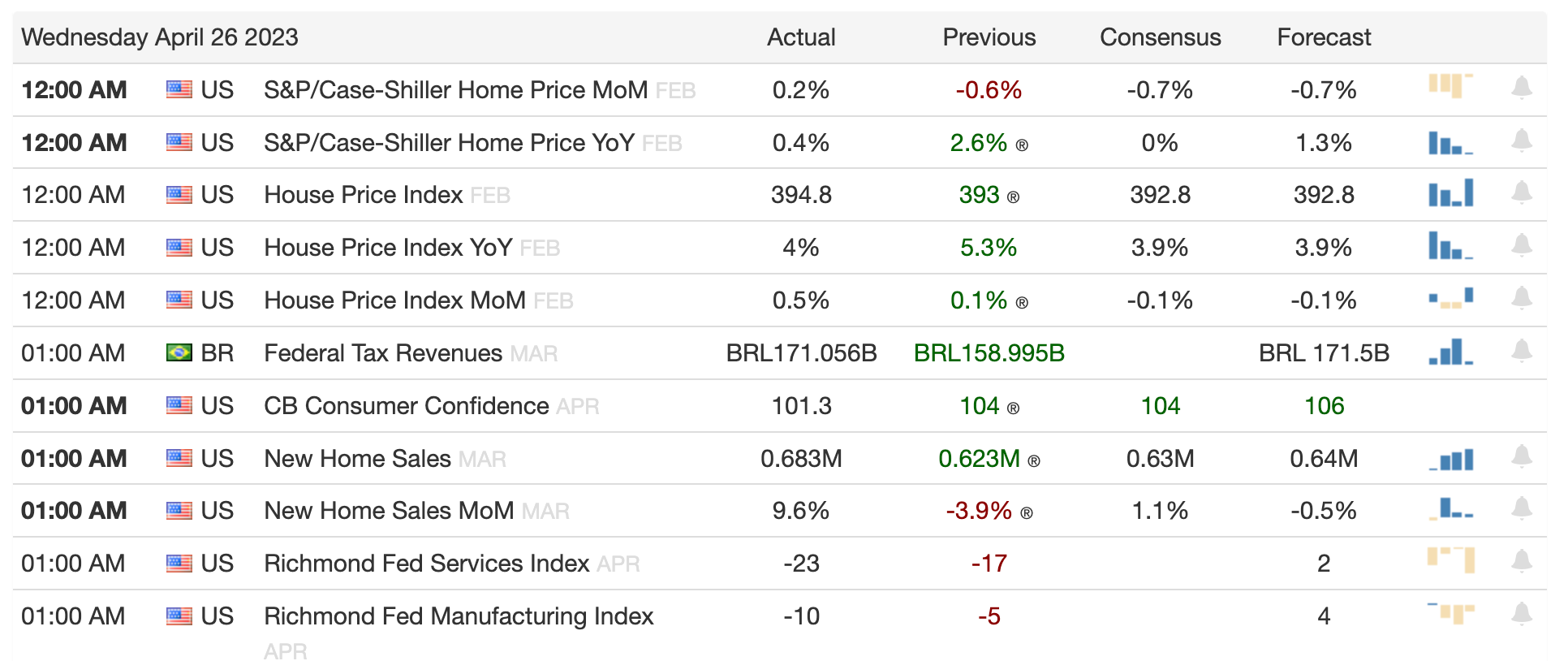

Here is a quick snapshot of this week’s US home price numbers. Despite a huge increase in rates, home prices are actually up because rents are rising quickly and the replacement cost of residential housing is rising too, providing a floor.

We’ve written about this extensively over the past few months and I’m now starting to see this divergence between residential and certain segments of the commercial market playing out. My March predictions are starting to materialise nicely.

While many previously expected pain to the banking system from residential housing, my focus has always been the impact and implications on the commercial market because of completely different factors driving valuations.

First some quick notes on valuations.

Commercial valuation process

Residential values are fairly transparent and because of the large volume of smaller sales, we tend to get a better read on movements. Commercial property is completely different, with less frequent and larger sales. We also have different valuation methodologies across different geographies.

From my understanding, listed US commercial assets are held at cost on their balance sheet and aren’t marked to market. Values only become relevant in unlisted vehicles or when listed companies have loans due for renewal, whereby lenders will dictate lending based on market value. So it’s a bit of a mixed bag.

According to Bloomberg, around US$92bn of US commercial debt will mature this year. Something will definitely start to happen in the next few months and while listed players can probably insulate themselves, there will be a recapitalisation process that starts soon.

But even if the US manages to insulate its commercial property problems, it doesn’t mean they won’t appear elsewhere.

The UK is probably the best placed given they have a different valuation culture. As one of my good friends recently put it to me, the “UK has a self-respecting profession of valuers” known as The Royal Institution of Chartered Surveyors (RICS).

This means that commercial property valuations often include a discounted cashflow method (DCF), which is very similar to the way companies and other finite assets are valued.

Australia is generally in a different situation, where commercial values are usually based on comparable sales and cap rates. This means that the market is sensitive to short term transactions. If the building next door sells for a 20% discount to last year’s prices, that can mean your building is 20% less in value too.

Cap rate valuations are also very sensitive to interest rate movements. All other things being equity, going from a 4% to 5% cap rate can impact valuations by 25% (1/4) whereas the impact on a DCF valuation will be much less.

From my understanding, Europe is very similar to Australia and has a lot more leverage. That’s where I see the biggest risk, particularly to European office exposure and the leverage from a very fragile European banking system.

We all saw that play out in March when one of Europe’s biggest and best known banking names — Credit Suisse — collapsed in a matter of days.

Office not yet opportunistic enough

Another very simplistic way I look at office is by seeing what the largest and best fund managers are doing. Blackstone’s recent US$30bn fund-raising (Blackstone Real Estate Partners X), while opportunistic in nature, is still shy of office and instead focused on logistics, rental housing, hospitality, lab office and data centers.

It’s not to say that office will never become opportunistic, it’s just that office is not opportunistic enough at this moment in time. There needs to be more pain and a revaluation process before it becomes opportunistic enough for the smart money sitting on the sidelines.

Office real estate reminds of television companies 10-15 years ago. Many were trading well below their book value, often below the value of their broadcast licenses. But the structural headwinds were so large that eventually those book values meant little as streaming services like Netflix and YouTube completely took eyeballs away from traditional TV and broke up their business models.

I understand that real estate is different, there is a tangible value, not just intangible values. I just think that the tangible value is well below what is currently sitting on balance sheet assumptions. Perhaps there is a 5-10 years write down process required before we can get to the point of measuring true value and replacement cost.

It’s a value trap and one that has a lot of financial risk attached to it. There are a lot more financial institutions exposed to office and retail than there were exposed to television companies.

A Mexican standoff is a confrontation where no strategy exists that allows any party to achieve victory. Any party initiating aggression might trigger their own demise. At the same time, the parties are unable to extract themselves from the situation without suffering a loss.

The losses are coming and given the size and nature, I believe financial stability will become more important for central banks in the coming few months. That will keep interest rates from moving up much further, for the time being.

My March predictions remain unchanged.

Peter Esho is an economist and Founder of Esho Group. He has 20 years of experience in investments and markets.