Stock prices supported by still strong earnings

One of the most important factors we look at during the stock market earnings season in the United States is the earnings beat rate. This measures the percentage of companies who report earnings above expectations. The key here is reality vs expectations.

Stock markets are driven by expectations of the future, not necessarily the situation on the ground or past performance. Earnings expectations are what moves the needle.

Despite consecutive interest rate increases, US companies have so far reported a 66% beat rate for the most recent earnings quarter. Of the data compiled, some 959 companies beat while 501 missed earnings. Most of the large companies that missed are down slightly in their stock price movement. For example, Boeing missed by a large factor, but its share price is relatively flat.

Over the past few weeks we’ve been writing about the better than expected economy being able to withstand rising rates. We wrote last week about inflation driven by strong economic activity and a hot jobs market.

Corporate earnings are reaffirming our view and as long as companies continue to meet expectations, it’s unlikely to cause the stock market to decline by a significant factor. No crash here.

The recession that everyone was expecting hasn’t showed up in corporate earnings yet…not has it shown up in retail, employment and GDP numbers so far in the United States.

There are cracks starting to emerge else, like the UK, Canada, Europe and Australia. Japan’s economic numbers this week were softer than expected. But those cracks are minor and the US economy is still sailing in an upward path.

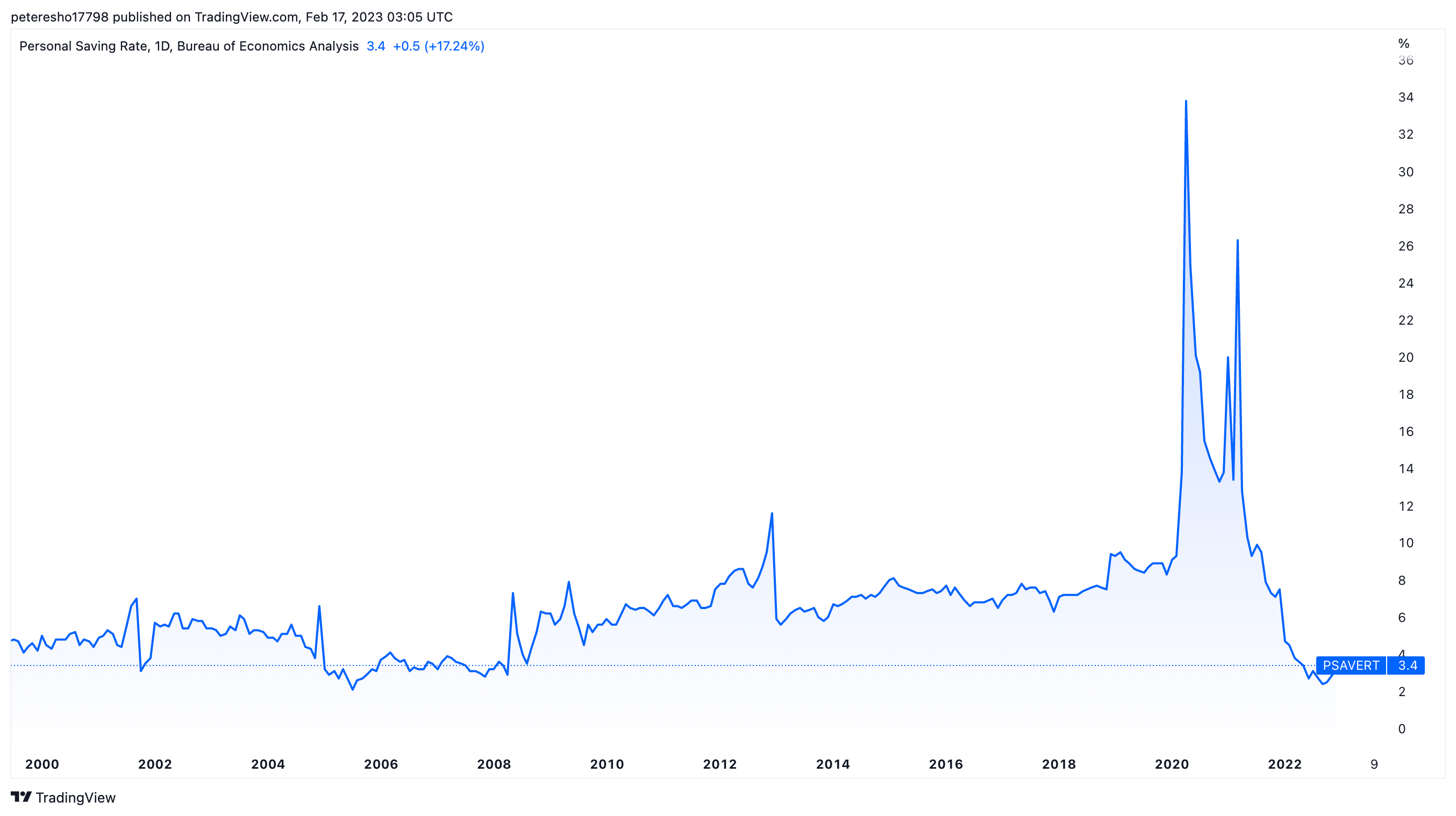

However, one of the most important things to watch is the personal savings rate. Consumers built up their savings during the pandemic but have been drawing down ever since. Rising rates have been partially offset by strong savings, but at some point, the rubber will hit the road as those savings are drawn down further.

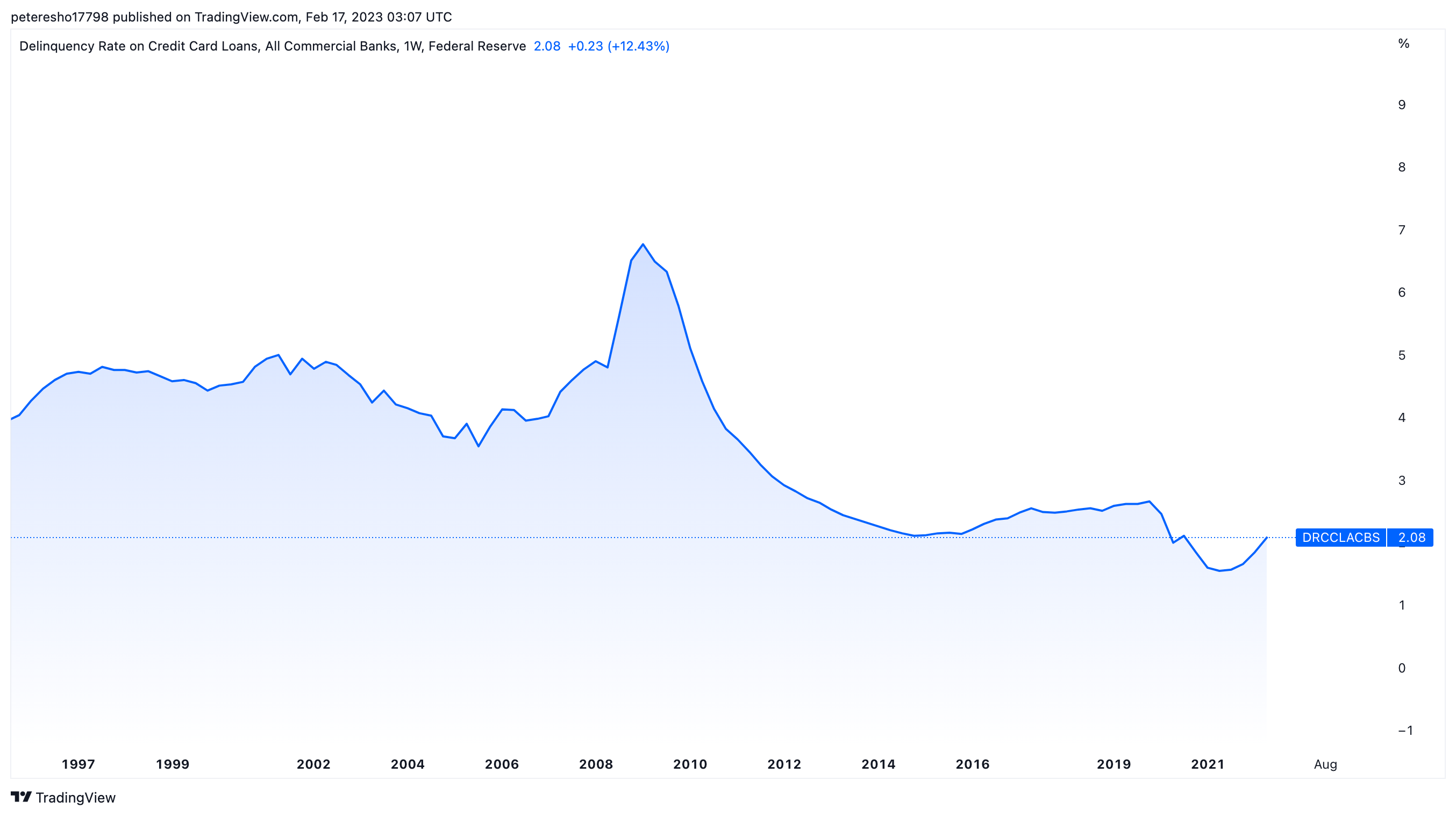

Credit card delinquencies (defaults) are another good forward indicator. They have been ticking up in recent months but nowhere near levels we’re used to seeing during a recession. The chart below shows US credit card defaults — still very low.

The lesson is this—sometimes in markets we tend to await confirmation of an event which we expected to occur, but it actually doesn’t. We miss the forest for the trees. While most have been under the assumption that a recession imminent and the stock market will collapse, the data suggests otherwise.

Corporate earnings are set to rise

A 66% beat rate for US stocks is clearly above expectations, despite consecutive interest rate rises. But the problem for the stock market is that with rising rates, company earnings need to continue rising to justify current valuations. The S&P500 and Dow Jones are current trading on price to earnings ratios of around 20x. That implies a 5% earnings yield, when inverted.

While traditionally not expensive, it’s hard to justify a 5% stock market yield when short term treasuries are yielding around 4.5%, some slightly higher. Most investors will tell you that the “stock vs cash premium” is too low, and the stock market will inevitably need to fall.

But there is another possible explanation.

If corporate earnings have the potential to grow, the current valuations can be justified and the “stock vs cash premium” is only temporarily narrow. The economy and corporate earnings could be in for some significant earnings growth, despite rates dampening activity. We believe this is now the base case forming for US stocks.

We need to keep in mind that the US economy is in an extremely strong economic position and rising rates are a response, not the reason, to be investing. A strong US dollar is likely to persist for most of the year which means earnings from multinational corporations are likely to stay strong.

Stock markets have found somewhat of a bottom in recent weeks and now forming a base which will be driven by earnings. The recent reporting season shows that earnings haven’t yet collapsed and the state of corporate America is in good shape. We think the picture is similar around the world, except for Asia, which is somewhat lagging a little behind.

Another thing we’re watching closely is the price large corporations are paying for their debt. We look at factors such as credit default spreads, which have recently narrowed and show strong demand for corporate debt. You don’t normally see this occurring when investors are worried about a recession or looming collapse in economic activity.

So the fact that large corporations have demand for their debt among lenders is another positive sign.

If you’ve been sitting on the sideline waiting for stock markets to bottom, now might be a good time to add to your portfolio. Our preference remains the S&P500 due to the diversified nature. It’s unclear if tech stocks have bottomed, due to their speculative nature and usually absence of earnings. So it’s best to play it safe with industrial exposure driven by fundamentals.

Outside the US we continue to like exposure to emerging markets. We also see value in Japan, which is set to deliver a new central bank governor in April, who might be able to shake up the current loose monetary policy situation. Our focus next week will be on Australia and the impact of recent commodity price moves.

Each week we use classical artwork in our thumbnail links as a source of inspiration. See this week’s artwork here.