Rate rises if pushed too far will cause cracks

We read with interest comments from ANZ Bank CEO Shane Elliot over the weekend, saying that future rate rises will hit borrowers harder and differently than recent rises.

The incremental impact of rate rises has somewhat been absorbed by the major Australian banks so far, which shows that borrowers are in a strong position.

But Elliot’s comments carry significant weight because the past isn’t necessarily a good guide for the future. Incremental rate rises beyond a certain point will push borrowers to the edge and that could open up larger balance sheet problems for the banks.

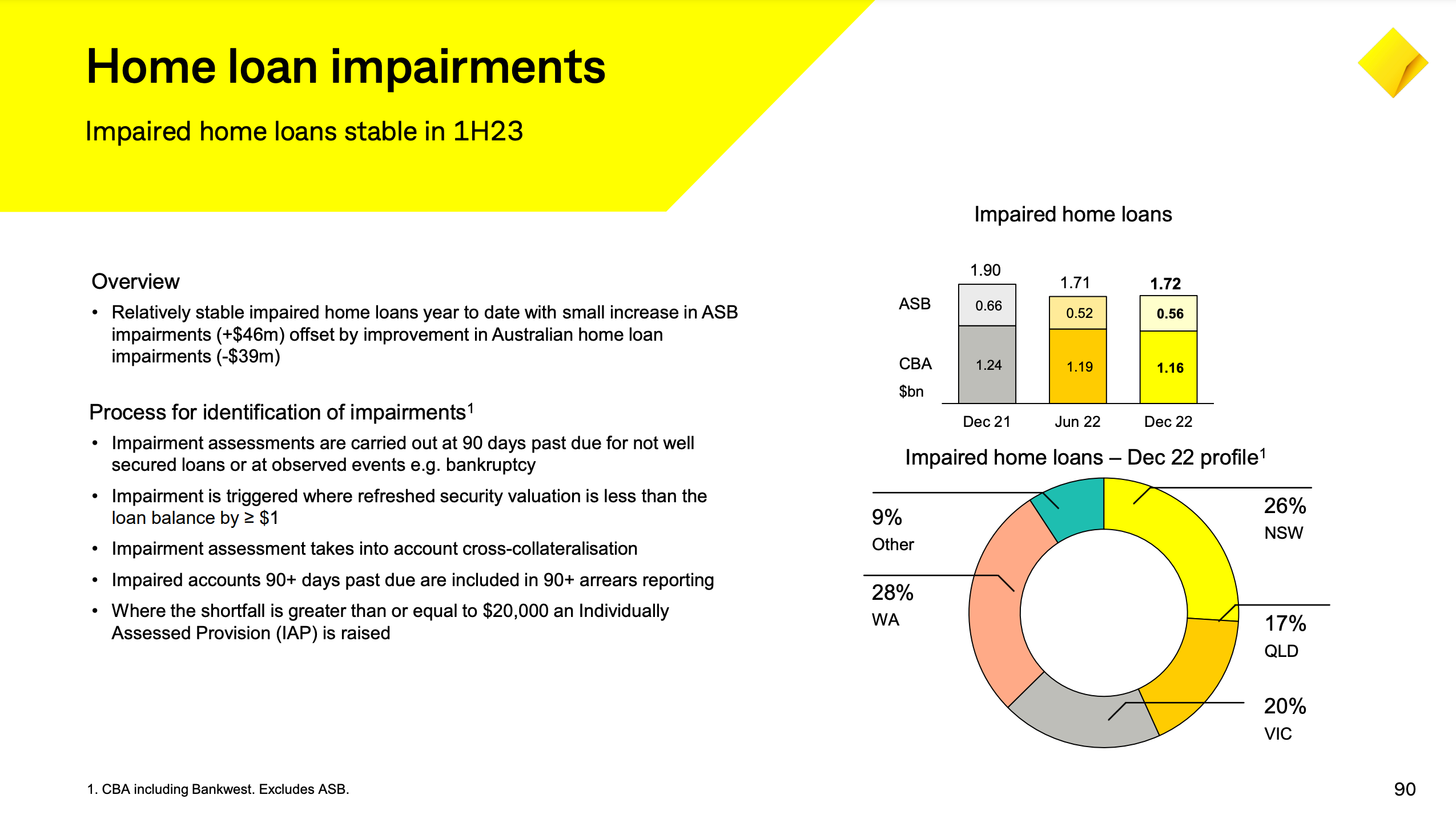

Commonwealth Bank’s recent earnings report disclosures showed impaired loans are at very comfortable levels despite 9 consecutive interest rate rises. There’s no significant pain at the moment.

But at some point, borrowers will start to eat into their saving buffers and the consequence will be a large fall off in discretionary spending. We don’t think rate rises will cause any significant real estate price declines because as we have written for many months, the supply pipeline and availability of homes, both existing and new, is very low.

Building permits and new home sales and approvals hit new lows last week, falling more than expected.

Many market economists have pointed to a looming interest rate cliff, where a portion of fixed rate loans will mature and reset to higher rates. But what many have missed is that there is another cliff out there in the market, a rental cliff, which has seen maturing rents reset at 20-40% higher levels, providing relief to out of pocket investors.

Elliot’s comments confirm our thesis, as noted by The Australian saying “He highlighted a risk that if buffer rates stayed at current levels they would “lock more people out” of the mortgage market, including those refinancing and first-home buyers.

Our underlying thesis remains that rising interest rates in Australia and to some extent Canada, will hit discretionary spending hardest, with modest impacts to housing, given very tight supply. The numbers so far seem to support that view.

We expect the RBA to raise rates by another 25 basis points tomorrow, however there could be some word changes in the statement that point towards cracks starting to appear in consumer spending later this year. That might open the door for a pause.

The bond market supports this view. Yields on 2 year Aussie bonds have hit their triple top cap of 3.65-3.7% and come off again. A sign that we may have peaked for the time being.