Opportunities to watch once the US dollar softens

While most of the market and investors are focused on interest rates, there’s another parallel story unfolding that will potentially cause a big shakeout in 2023. Rising US interest rates, which don’t look like they’ll stop anytime soon, have seen the US Dollar (USD) rise to record high levels against most major currencies.

Higher rates in the US means money flows into US securities, chasing higher returns, and out of lower interest rate economies. A weak currency is ok for an export economy like Australia or Canada because it makes exports more competitive.

But you don’t want your currency to fall too hard and too strong because that also brings with it many other pains, like imported inflation and higher debt repayments for situations where debts are dominated in USD.

Imagine having borrowed $1bn in US debt and your currency slides by 20% in a year against the USD. Your entire solvency position as a business or organisation can change just on that very move.

Here’s what the US Dollar Index looks like, a measure of USD against its largest trading peers.

Japan is a perfect example of an econmy struggling to cope with a higher USD. According to Reuters, Japan spent a record $42.8 billion on currency intervention in October to prop up its currency. This is usually done by selling foreign currency and buying the yen.

The strategy has so far worked to stop the USD from rising above 150 Japanese Yen (JPY). But its a huge price to pay. It’s not necessarily that the JPY is weak, instead its the strength in the USD. Here’s the USD against the JPY going back to 2005. We’re near historic high levels.

Japan has more than $1 trillion in foreign currency reserves, so it can afford to keep up its intervention. But not forever. At some point, things will break. Other economies like India are worse off and will struggle. Here’s the depreication of the Indian Rupee against the US dollar over the same time period.

The rising USD also causes headaches for many American companies who have global operations. When they translate their earnings back to their home country, they end up converting into less USD.

Take for AirBNB for example, a platform which hosts guests all around the world. AirBNB’s third quarter net income was 15% lower due to currency translation impacts. It’s revenue was 7% lower. Pfzier similarly saw a $1bn sales impact from a rising USD compared to other major currencies.

The Ex-US contrarian trading opportunity

But like every trend in markets, there is always an opportunity. We look for oversold or overbought situations to form contrarian thoughts and opinions. As the Book of Ecclesiastes teaches us in chapter 3, there is a season for everything. The world moves in cycles and markets are no different.

Emerging markets stocks are trading at record low levels relative to US stock markets. A lot of this discount has been due to the stronger US dollar. But there are a lot of great companies around the world that, at some point in the near future, will go through a rerating once the US economy goes into recession and the interest rate outlook starts to change.

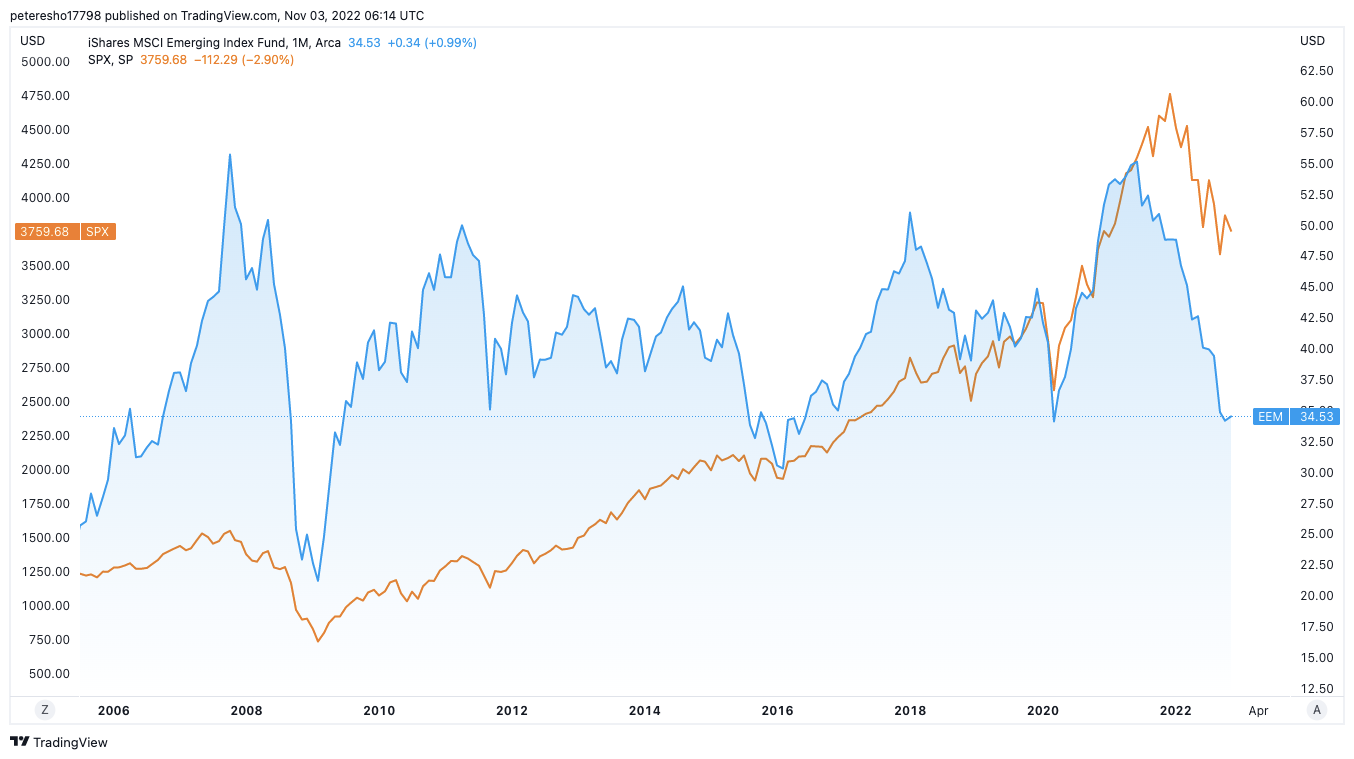

In our simple analysis, we look at the EMM (Emerging Markets ETF) and compare it with the US S&P500 index. Over the past 17 years, emerging markets have regularly traded at big premiums compared to the US market. The current post-pandemic period is an anamoly.

Investment flows into emerging markets have been dampened recently due to politics and pandemics. Russia, India and Saudi Arabia all have precarious political relationships with the West.

China has been in a lockdown for the past two years and before that we had the ongoing trade war with the United States. Many of the key constituents in emerging market ETFS are based in Asia. So again, there might be some more reasons here to explain the price gap.

But again, things change, markets move in cycles and in a couple of years, these reasons could have compeltely disappeared.

China will eventually transition from its zero covid policy and start to open up. We don’t know when, but we do know that eventually it cannot sustain a lockdown with the rest of the world for too much longer.

The bottom line

Interest rates are likely to continue rising in the US over the next year. The Fed is on a mission to kill inflation, they’ll kill many parts of the economy in that process.

But like all battles, sometimes the ends justify the means. Its hard to bet against the US dollar in the short term, but now is the time to be brave and look forward medium term opportunities.

Ultimately economic growth and market appreciation is driven by two big factors — demographics and productivity. Wars are fought to either increase the population (think the conquering of India for example) or to increase resources in order to lower input costs for productivity growth (oil wars).

The emerging world has population growth and with decentralised technology only expected to increase in adoption, we can follow through with the assumption that productivity is on the up there too.

Emerging markets are out of favour and trading at a big discount, mainly due to short term forces, which will subside. So it’s time to start adding some ex-US exposures to your portfolio. It’s time to start betting against the US dollar.

Portfolio ideas include Ex US broad based ETFS. For stock indices, preference is Australia, Canada and UK. It’s still too early to look at industrial commodities, but if China does open quicker than expected, we could see higher energy and copper prices.