Global housing holding up despite higher rates

Many investors thought that rising interest rates around the world would crush real estate prices, particularly in highly leveraged markets. The data continues to confirm that while prices have come down, the real estate market continues to move into a “freeze” situation which we wrote about late last year.

The freeze is characterised by construction grinding to a halt and activity falling as uncertainty grips the markets. But prices declines remain limited due to falling supply. What we’ve seen across many developed markets is goods inflation still persisting in building costs and vendors being locked into their loans, due to a lack of alternatives.

One of the things we’re also starting to see in Australia is feedback from the real estate development industry that developers are now starting to increase their prices and delay project starts in order to make their feasibilities work.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

With bond yields continuing to rise last week and consensus building that rates will stay higher for longer, we now think that the freeze will continue and supply will take a huge hit over the coming few years.

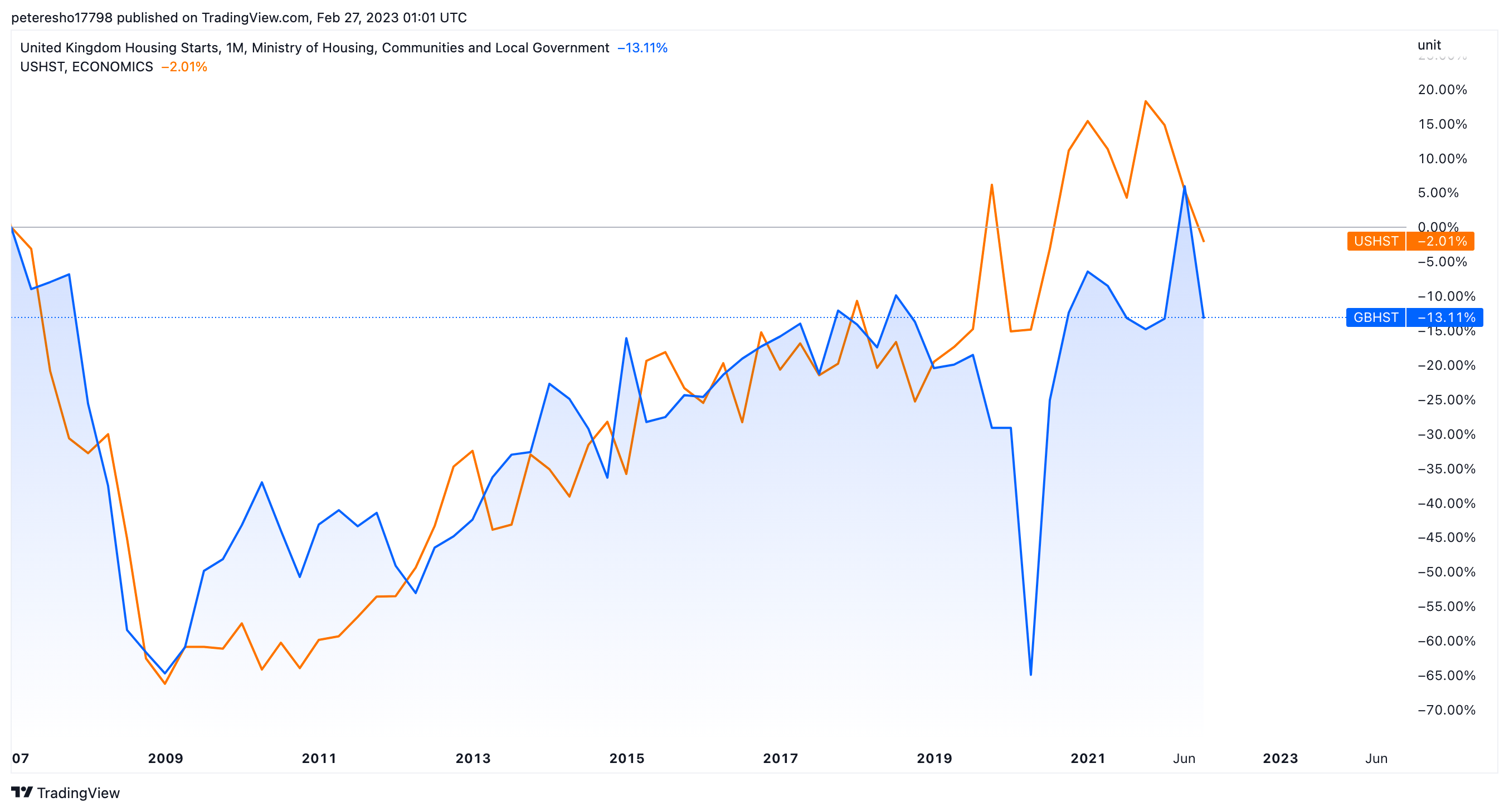

We ran a comparison between US and Australian housing starts a few weeks ago which shows that supply is falling. According to estimates, the UK today has a backlog of around 4.3m homes. This deficit would take at least half a century to fill even if the Government’s current target to build 300,000 homes a year is reached.

Tackling the problem sooner would require 442,000 homes per year over the next 25 years or 654,000 per year over the next decade in England alone. UK housing starts fell around 19% in the September quarter. We expect to see a similar moderation when December numbers are released in May.

The chart below compares US and UK housing starts since the 2008 housing crash, both markets have supply starting to trend lower.

The housing freeze narrative starts with lower supply and ends up with job losses in the construction industry. We haven’t yet seen these job losses, but they could feature in the data over the next few weeks and that will be our primary focus.

Editor’s Note: Our property analysis and insights are moving to a bi-monthly format where we will look at property trends and insights across a range of markets.